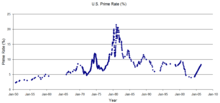

U.S. prime rate

In general, the United States prime rate runs approximately 300 basis points (or 3 percent) above the federal funds rate. The Federal Open Market Committee (FOMC) meets eight times per year wherein they set a target for the federal funds rate. Other rates, including the prime rate, derive from this base rate.

The most commonly recognized prime rate index is the Wall Street Journal prime rate (the WSJ prime rate), published in The Wall Street Journal. Unlike other indexed rates, the prime rate does not change on a regular basis; rather, it changes whenever banks need to alter the rates at which borrowers obtain funds. The WSJ defines the prime rate as "The base rate on corporate loans posted by at least 75% of the nation's 30 largest banks." It has been speculated though that this is no longer the real definition (and that the prime rate is simply the fed funds target rate + 3), because most corporate loans are indexed to LIBOR.

When 23 out of 30 largest US banks change their prime rate, the WSJ prints a composite prime rate change.

Uses

The prime rate is used often as an index in calculating rate changes to adjustable rate mortgages (ARM) and other variable rate short term loans. It is used in the calculation of some private student loans. Many credit cards with variable interest rates have their rate specified as the prime rate (index) plus a fixed value commonly called the spread.